How Can I Invest My Money In India

Whenever I talk to anyone about money and investing, I basically have the following guiding principle:

Save 3-6 months of living expenses, pay off all high-interest debt/loans and invest everything else.

Do I practice what I preach? Yes. I absolutely do.

The reason is that I believe that investing your savings into the market is the single greatest way to make your money "work for you" and if done consistently, is the easiest way (at least in my opinion) to achieve financial independence. My family has been doing it for 6+ years now and I think we've done pretty well. There's no secret sauce to investing, don't let financial advisors fool you, it's really as easy as setting up a recurring investment into "VOO" or "SPY" or whatever low-cost S&P 500 index fund, not touching it and doing this consistently for years. Yes, the market can be volatile and months like March 2020 can be scary as hell, or years like 2008 can be stomach-churning, but historically the market goes up and if you don't make any moves (i.e. DON'T PANIC SELL) during volatile periods, you'll most likely do just fine:

How We Manage our Finances

So my wife and I put our 3-6 months worth of living expenses cash into BlockFi (yields 9% but not FDIC insured) and M1 Finance's checking account (yields 1% and is FDIC insured). From a brokerage account perspective, we use Fidelity primarily because I really like their user interface, trading platform, research, etc. We also have an M1 Finance brokerage account as well as a Robinhood account.

I primarily use Robinhood to make weekly investments into 10 or so stocks as well as a few dividend ETFs. Yes, I make weekly investments into the market on Monday mornings largely because historically Monday is the worst performing day so I usually can dollar cost average into my positions at a lower cost basis. As I have written in my past entries, I invest solely in individual stocks which could mean an array of stocks and option plays.

From a retirement account perspective, we max out our Roth IRAs and 401ks on an annual basis. Where in our Roths, similar to our brokerage accounts, we invest solely in individual stocks (no funds). In our 401ks, since they don't allow individual stocks, we allocate around 85% or so into equities, mostly large-cap, so the S&P 500, but also allocate a significantly smaller amount to mid-cap/small-cap/international/REIT funds. The other 15% is in bonds or "cash equivalent" funds.

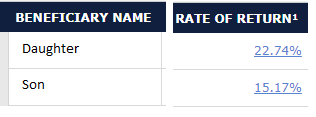

We also have Illinois 529 accounts for our kiddos which we do a monthly deposit to both kiddos. I noted that it's Illinois-specific since we get a tax deduction on our state income taxes for contributions. For my son, I just chose a target-date fund and for my daughter, I chose an asset allocation just to test the waters (funds not stocks), and interesting enough, it's outperforming my son's account. Probably won't always be the case, but it is for now.

Finally, I have several mining rigs that mine the cryptocurrency ethereum and I buy ethereum on a weekly basis on BlockFi.

Other Notes

- We live well below our means which enables us to invest a lot into the market.

- We invest in individual stocks because of the sheer outperformance vs. S&P 500 but nothing wrong with the S&P 500 (Read here and here)

- We generally save around 30-40% of our salaries and just about all of that goes into the market.

- We have a small amount of debt from the new cars that we bought this year at a 1.9% to 2.7% interest rate. I made a large down payment largely to minimize the monthly payment. Yes, I know this is not what I generally recommend in terms of handling debt since low interest rate debt should be kept due the opportunity cost of paying off the debt vs. investing. However, I did this largely to keep monthly cash expenses low and not wanting to be saddled with high fixed monthly cash obligations.

- We pay the majority of our expenses with a credit card. I'm not very points savvy, I just use the Chase Sapphire credit card since I can hoard miles for travel.

- Towards the end of every month, I'll download my credit card statement and input every expense item into an Excel spreadsheet and categorize it. Yes, I recognize this sounds ridiculous, but that's just how I've always handled my money. I'm willing to spend the hour every month to better understand where our salaries are going.

- We donate around 10% of our net income to ministries and charities we support. Recently I have been donating more stock than cash for the tax benefits.

- On the 1st day of the month, I do "month end" early in the morning to reconcile all bank accounts, brokerage accounts and to calculate net worth. I also download my brokerage statements to calculate YTD returns and track how it performs against the S&P 500.

This is how I budget, manage and invest my money on a daily/weekly/monthly basis. In all, I spend about 2-3 hours a month inputting and reconciling my expenses & accounts. I personally think everyone should spend at least an hour a month reviewing their accounts since it's helpful to know where your money is going and what it's invested in and evaluate if those investments are appropriate.

How Can I Invest My Money In India

Source: https://www.franklinkuok.com/how-i-manage-and-invest-my-money/

Posted by: morrissearenes.blogspot.com

0 Response to "How Can I Invest My Money In India"

Post a Comment